import numpy as np

import matplotlib.pyplot as plt

import climatecritters as cc

from climatecritters.model_critters.ebm import EBM0D

from climatecritters.utils import noise as cc_noise

import pyleoclim as pyleo

T_SPAN = (0, 500) # yearsNoise in Models — Three Injection Modes

Abstract

Three independent ways to introduce stochasticity differ fundamentally in where noise enters the dynamics. Noisy forcing feeds randomness through the model’s input; SDE integration (Euler-Maruyama, Heun-Maruyama, Milstein) injects it directly into the state update; post-integration noise simulates observation error without any dynamical feedback. This notebook compares all three approaches on EBM0D.

Keywords

noise, noisy forcing, SDE, Euler-Maruyama, Heun-Maruyama, Milstein, stochastic integration, observation noise, ensemble, EBM0D

Clean baseline

Run once; reuse throughout for comparison.

model_clean = EBM0D()

out_clean = model_clean.integrate(t_span=T_SPAN, y0=[255.0], method='RK45')

T_clean = out_clean.state_variables['T']

t_clean = out_clean.timeNoisy forcing

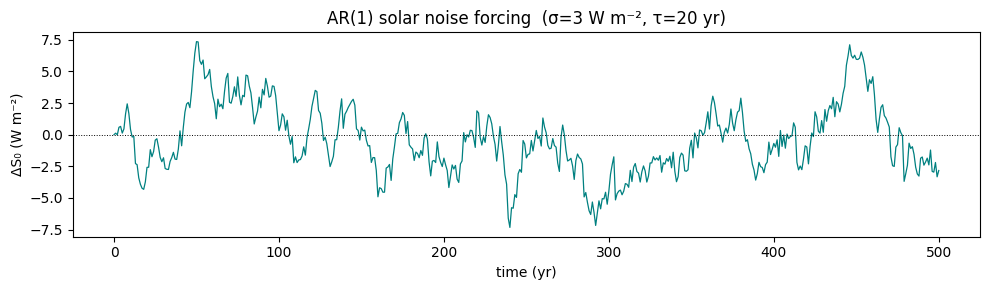

Wrap a stochastic process in a cc.Forcing callable and attach it with register_forcing. The noise is part of the input, not the state equations, so the model stays deterministic and the perturbation is inspectable.

Here: AR(1) noise added to S0 (the solar constant).

Always visualise the forcing before attaching it.

t_eval = np.arange(T_SPAN[0], T_SPAN[1] + 1, dtype=float)

# AR(1): σ=3 W m⁻², τ=20 yr

sigma_drive, tau_drive = 3.0, 20.0

rng_f = np.random.default_rng(0)

noise_vals = np.zeros(len(t_eval))

for i in range(1, len(noise_vals)):

alpha = np.exp(-1.0 / tau_drive)

noise_vals[i] = (alpha * noise_vals[i-1]

+ sigma_drive * np.sqrt(1 - alpha**2) * rng_f.standard_normal())

solar_noise = cc.Forcing(

lambda t, _t=t_eval, _v=noise_vals: float(np.interp(t, _t, _v))

)

# Visualise first

fig, ax = plt.subplots(figsize=(10, 3))

ax.plot(t_eval, noise_vals, color='teal', lw=0.9)

ax.axhline(0, color='k', lw=0.7, ls=':')

ax.set_xlabel('time (yr)'); ax.set_ylabel('ΔS₀ (W m⁻²)')

ax.set_title('AR(1) solar noise forcing (σ=3 W m⁻², τ=20 yr)')

plt.tight_layout(); plt.show()

model_noisy_f = EBM0D()

model_noisy_f.register_forcing('S0', solar_noise, 'additive')

out_noisy_f = model_noisy_f.integrate(t_span=T_SPAN, y0=[255.0], method='RK45')

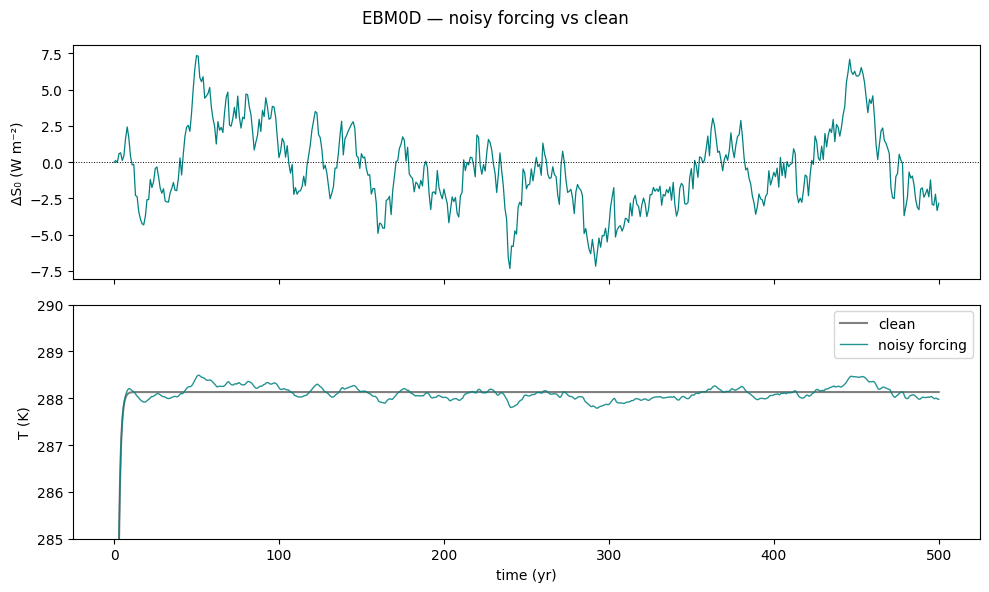

fig, axes = plt.subplots(2, 1, figsize=(10, 6), sharex=True)

axes[0].plot(t_eval, noise_vals, color='teal', lw=0.9)

axes[0].axhline(0, color='k', lw=0.7, ls=':')

axes[0].set_ylabel('ΔS₀ (W m⁻²)')

axes[1].plot(t_clean, T_clean, color='gray', lw=1.5, label='clean')

axes[1].plot(out_noisy_f.time, out_noisy_f.state_variables['T'],

color='teal', lw=1.0, alpha=0.85, label='noisy forcing')

axes[1].set_xlabel('time (yr)'); axes[1].set_ylabel('T (K)'); axes[1].legend()

axes[1].set_ylim((285,290))

fig.suptitle('EBM0D — noisy forcing vs clean')

plt.tight_layout(); plt.show()

Figure. The noisy run tracks the forcing with a lag set by the thermal inertia. The perturbations never drive the model to a new equilibrium because the noise is zero-mean and the heat capacity keeps the system well-damped.

Noise during integration

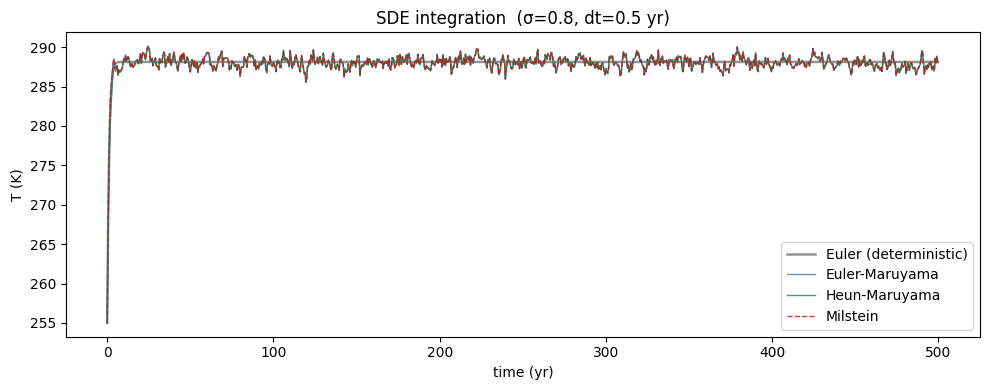

SDE integrators inject noise at every timestep: \(dT = f(T)\,dt + \sigma\,dW\).

To use them: 1. Set model.sde_noise = lambda t, state: noise_scale_vector 2. Call integrate(..., method='euler_maruyama') — or heun_maruyama (strong order 1.0) or milstein (strong order 1.0, multiplicative noise) 3. Pass kwargs={'dt': ..., 'random_seed': N} — dt is required

heun_maruyama is the default recommendation: better accuracy than euler_maruyama at the same dt, with no extra cost for additive noise.

SIGMA_SDE = 0.8 # K yr⁻⁰·⁵

DT_SDE = 0.5 # yr

def sde_noise_fn(t, state):

return np.full_like(np.asarray(state, dtype=float), SIGMA_SDE)

# Deterministic Euler baseline vs three SDE methods

configs = [

('euler', {}, 'gray', '-', 'Euler (deterministic)'),

('euler_maruyama',{'random_seed': 0}, 'steelblue', '-', 'Euler-Maruyama'),

('heun_maruyama', {'random_seed': 0}, 'seagreen', '-', 'Heun-Maruyama'),

('milstein', {'random_seed': 0}, 'firebrick', '--', 'Milstein'),

]

runs_sde = {}

for method, extra_kw, color, ls, label in configs:

m = EBM0D()

if method != 'euler':

m.sde_noise = sde_noise_fn

out = m.integrate(t_span=T_SPAN, y0=[255.0], method=method,

kwargs={'dt': DT_SDE, **extra_kw})

runs_sde[label] = (out, color, ls)

fig, ax = plt.subplots(figsize=(10, 4))

for label, (out, color, ls) in runs_sde.items():

lw = 1.8 if label == 'Euler (deterministic)' else 1.0

ax.plot(out.time, out.state_variables['T'],

color=color, ls=ls, lw=lw, alpha=0.85, label=label)

ax.set_xlabel('time (yr)'); ax.set_ylabel('T (K)')

ax.set_title(f'SDE integration (σ={SIGMA_SDE}, dt={DT_SDE} yr)')

ax.legend(); plt.tight_layout(); plt.show()

Figure. For additive noise (σ independent of state) Milstein’s correction term is zero, so Heun-Maruyama and Milstein give identical trajectories at the same seed. All three converge to the same neighbourhood of ~288 K — noise is zero-mean, so it doesn’t shift the attractor.

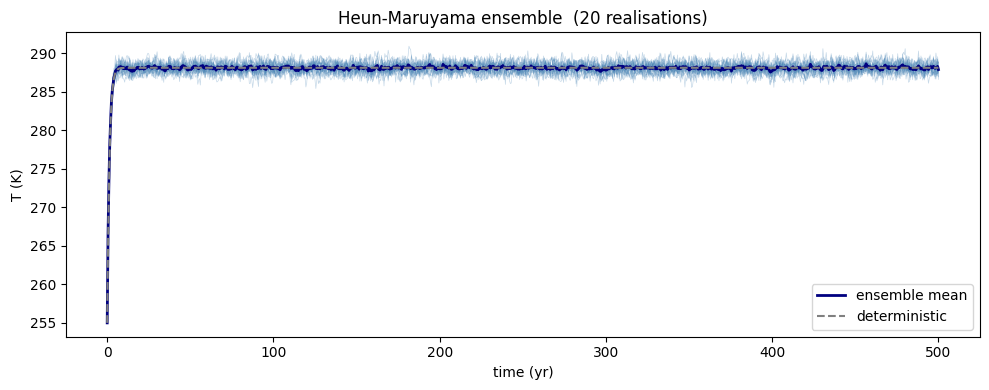

# Run an ensemble to characterise spread

N_ENS = 20

ens_T, ens_t = [], None

for seed in range(N_ENS):

m = EBM0D(); m.sde_noise = sde_noise_fn

out = m.integrate(t_span=T_SPAN, y0=[255.0], method='heun_maruyama',

kwargs={'dt': DT_SDE, 'random_seed': seed})

ens_T.append(out.state_variables['T'])

if ens_t is None:

ens_t = out.time # time axis from the SDE runs

ens_arr = np.array(ens_T)

# Trim the clean reference to the same length if needed

T_clean_ref = T_clean[:len(ens_t)] if len(T_clean) > len(ens_t) else T_clean

t_clean_ref = t_clean[:len(ens_t)] if len(t_clean) > len(ens_t) else t_clean

fig, ax = plt.subplots(figsize=(10, 4))

for row in ens_arr:

ax.plot(ens_t, row, color='steelblue', lw=0.5, alpha=0.3)

ax.plot(ens_t, ens_arr.mean(axis=0), color='navy', lw=2, label='ensemble mean')

ax.plot(t_clean_ref, T_clean_ref, color='gray', lw=1.5, ls='--', label='deterministic')

ax.set_xlabel('time (yr)'); ax.set_ylabel('T (K)')

ax.set_title(f'Heun-Maruyama ensemble ({N_ENS} realisations)')

ax.legend(); plt.tight_layout(); plt.show()

Figure. Ensemble mean converges to the deterministic equilibrium; spread is largest during the fast transient when the gradient is steepest.

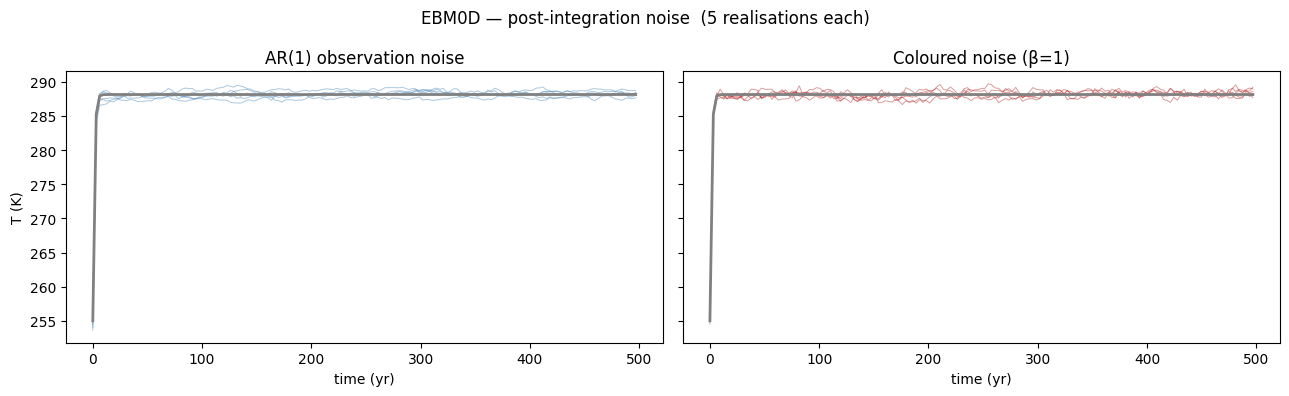

Noise post-integration

Run the model cleanly, then add noise to the output series with climatecritters.utils.noise. Use this when the noise represents observation error or proxy noise rather than intrinsic variability — the dynamics stay deterministic and reproducible.

ts_clean = pyleo.Series(time=t_clean, value=T_clean,

time_name='time', time_unit='yr',

value_name='T', value_unit='K', label='deterministic')

# RK45 produces irregular timesteps — interpolate to regular grid before

# generating surrogates (ar1sim requires evenly-spaced time)

ts_clean_reg = ts_clean.interp()

t_reg = ts_clean_reg.time

T_reg = ts_clean_reg.value

# AR(1) surrogates matched to the signal's autocorrelation

surr_ar1 = cc_noise.from_series(ts_clean_reg, method='ar1sim', number=5, seed=1)

# Pink noise (β=1) from parameters

surr_cn = cc_noise.from_param(method='CN', noise_param=[1], length=len(t_reg),

time_pattern='specified',

settings={'time': t_reg}, number=5, seed=2)

fig, axes = plt.subplots(1, 2, figsize=(13, 4), sharey=True)

for ax, surr, color, title in [

(axes[0], surr_ar1, 'steelblue', 'AR(1) observation noise'),

(axes[1], surr_cn, 'firebrick', 'Coloured noise (β=1)'),

]:

ax.plot(t_reg, T_reg, color='gray', lw=2, label='deterministic', zorder=3)

for s in surr.series_list:

noisy = T_reg + 0.5 * (s.value - s.value.mean()) / s.value.std()

ax.plot(t_reg, noisy, color=color, lw=0.7, alpha=0.45)

ax.set_xlabel('time (yr)'); ax.set_title(title)

axes[0].set_ylabel('T (K)')

fig.suptitle('EBM0D — post-integration noise (5 realisations each)')

plt.tight_layout()Time axis values sorted in ascending order

{'label': 'deterministic'}

{'label': 'deterministic'}

{'label': 'Power-law surrogates ($S(f) \\propto f^{-\\beta}$) #5'}Figure. Both panels converge to exactly the same deterministic equilibrium — post-integration noise does not feed back into dynamics. AR(1) produces slower meanders; pink noise adds spectral richness across all scales.

Which approach to use?

| Noisy forcing | Noise during integration | Noise post-integration | |

|---|---|---|---|

| Feeds back into dynamics | ✓ (through input) | ✓ (on state) | ✗ |

| Deterministic model preserved | ✓ | ✗ | ✓ |

| Physical interpretation | Boundary/external forcing | Intrinsic variability | Measurement / proxy noise |

| Reproducibility | Pre-draw + wrap | random_seed kwarg |

seed in from_series/from_param |

| Requires SDE integrator | ✗ | ✓ | ✗ |